How do I handle high inflation?

Higher inflation means almost everything is more expensive. And that means our money isn’t going as far. So how do you survive?

Start by not doing these 4 things:

Don’t panic…even if you’re feeling overwhelmed

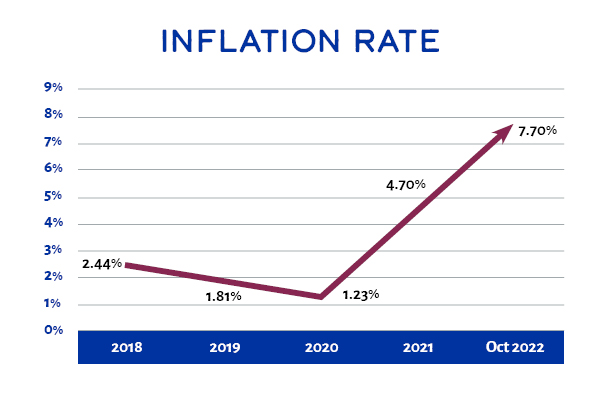

When the cost of groceries has gone up anywhere from 13% to 24%1, being told “don’t panic” is like being told you need to stop buying coffee if you ever want to buy a house. In other words: frustrating.

But the fact is: inflation is a part of global economics. It has happened before, it will happen again. There should be some comfort in this. People have faced high inflation before and worked through it. You can, too (even if you don’t feel like you’re managing it well right now).

“…everyone’s life plans can be affected by inflation” Entrepreneur Magazine(Opens in a new window)

Panic can lead to money decisions you’ll regret. So, even though you’re stressed, take a deep breath and step back. One of the best things you can do for yourself is talk to your bank or credit union or your financial advisor. They have the knowledge and resources to guide you through higher-inflation environments.

Achieve financial resilience

You can make your money (and your

peace of mind) resilient to periods of

financial hardship. Find out how in this guide.

Get Your Guide

But don’t pull your money out of savings accounts, either

Unless you’re facing an emergency or unexpected expense, do your best to keep your savings account intact. It’s especially important during periods of inflation. Businesses facing lower sales are often forced to reduce staff. And a healthy savings account will help you manage a potential loss of income. Beyond that? It also just brings peace of mind.2

One exception? If you’re using money to fund a higher-return money market or certificate. Some savings tools, including shorter-term certificates and money markets, could earn you higher returns. With variable rates – or a locked-in higher rate – putting money into these types of accounts could help you build a buffer. Don’t cut yourself short just to invest in other options, though. You’ll want to keep as much money in your savings account as possible.

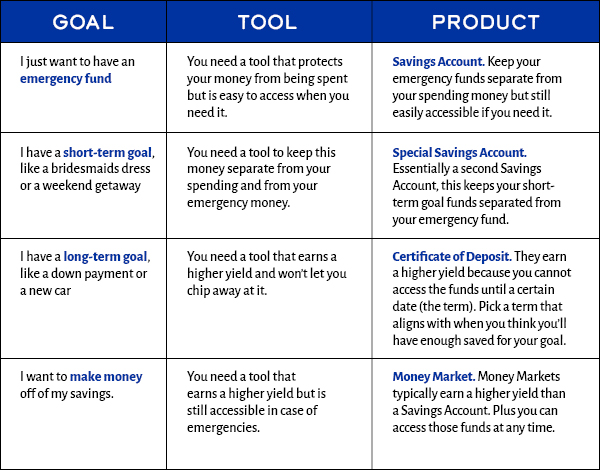

Ways to Save Money According to Your Goal

Avoid those tempting easy-money schemes

When money gets tight, we get emotional. And those emotions can sometimes cloud our judgment. In fact: research suggests that financial stress impairs our ability to make rational decisions.3 So when we’re faced with higher prices at every turn, we start to look for ways out.

And that’s where easy money scams start to look good.

People who perpetuate easy-money offers understand this. And that’s why they highlight how “fast” and “simple” their money-making solution is. The most important thing to do? Step back.

Top easy-money scams to avoid

Secret shopper

The ultimate easy-money scam. All you need to do is rate a store! Here’s the problem: fraudsters rely on urgency to scam you out of your own money. Here’s how it works: you apply for a job or post your resume online. An email or envelope comes your way with an offer for a position as a secret shopper. A check is included. And you’re instructed to cash the check as soon as possible, keep a sum for yourself, and use the rest to shop at designated stores. Your final task? Test the local Western Union and wire the remaining money back. Complete the enclosed satisfaction form. Easy money, right? Wrong. The fraudsters urge you to cash the check and do your secret shopping right away because they know the check is bad. But it won’t bounce before you’ve already done your “job” and wired them money.

Think about this: anyone who offers to hire you without an interview should immediately make you suspicious.

The

latest scans to avoid

Get the scoop on the latest scams

to avoid from MHV’s VP of Asset Protection.

Read the Article(Opens in a

new window)

Money mules

If someone asks you to deposit cash into your account, then transfer it to them digitally, don’t. Even if they entice you with a sweet 10% cut. Or if they beg you saying they work for cash only and are going to get hit with taxes if they deposit the funds. Think about the fact that these funds may have been obtained illegally, and now they’re being deposited into your account! Do you really want your name and account information connected to that? Why would someone you don’t know offer to deposit funds into your account. Sure, that 10% sounds good when you are struggling with bills, but it simply is not worth breaking the law.

Work from home scams

There’s no doubt that legitimate work-from-home opportunities exist, especially in this post-pandemic world. But unfortunately, that also makes it easier for illegitimate ones to hide. And with how easy it is to build a website, it can be hard to differentiate the real from the fake. Head to review sites to search for feedback on any opportunities before you dive in. A big red flag? If the company requires you to send them money – or share your account information – so they can purchase office equipment for you. If the alleged company sends a check and asks YOU to purchase a laptop and then ship it to them to have software installed you’ll most likely never see the laptop again. Or if they ask you to send money to someone who will then ship you a laptop and other office supplies, you’ll never see that money or hear from them again.

Organize your debt

Get a handle on your debt to stay in focus and resilient during periods of inflation. Start with this download to organize your payments. Get my Download(Opens in a new window)

MLMs

With their “work anytime” taglines, multi-level marketing companies (MLMs) appeal to busy people struggling to make ends meet. But the FTC warns that the income claims often made by these companies are far from the truth.4 In fact, people who join MLMs often end up losing money because they’re pressured to buy their company’s products. So while it may sound like a golden opportunity, things that are too good to be true often are just that…too good to be true.

Debt relief programs

It’s not necessarily a money-making scheme, but these programs rely on people’s feelings of financial helplessness to make money. Debt relief programs promise to work with creditors to pay your bills off…for a fee. The problem is that creditors don’t have to work with debt relief companies. So now you’re out the money to pay for the program and still have to pay your bills. Sometimes there is a reduced payment, but not enough to offset the fee. And sometimes, according to Experian, the portion that is forgiven can be considered taxable income.5 Instead of turning to debt relief programs to help save money, work directly with your lenders or creditors. Many have hardship programs available.

“I

feel overwhelmed by my bills.”

Is debt

consolidation better than a debt relief program? Find out in this

9-minuted video.

Watch the Video(Opens in a new window)

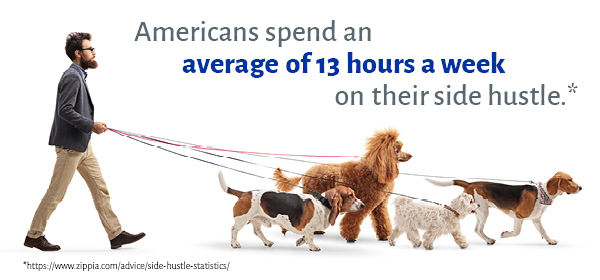

Legitimate side-hustles

Not every side-hustle is bad. And there are some great

money-making opportunities

that fit into an already busy schedule. It’s hard to give up your free time, but if

inflation is making you panic about your finances, setting up additional income

could help relieve some stress.

Dog walking or pet sitting

Offering dog walking or pet sitting services to friends, family, and neighbors is

one way to boost your income – and it doesn’t require much investment on your

part.

Survey/website

testing

While some of these are scams, there are legitimate companies that offer payment for reviewing websites or taking surveys. Do your research before signing up. And keep in mind: you shouldn’t have to pay to join and can work as needed.

Freelance work

If you have extra time, pick up freelance work to help bring in additional income. If you already work, check with your Human Resources representative to make sure there are no non-compete clauses or other policies that may limit freelance work.

Don’t pile on the credit card debt

It’s a lot easier to reach for your credit card when prices soar. It hurts less than seeing your checking account balance erode. But racking up credit card debt during periods of high inflation is a double-whammy.

First, you’re going to have to pay that money back. And if you’re already feeling a financial pinch, adding a higher monthly payment isn’t going to help. And credit cards often have a variable rate, meaning as the federal reserve raises the prime rate, your card’s rate will go up, too. A higher interest rate means a higher monthly payment. And a higher payment is something you want to avoid as everything else gets more expensive. (Inflation doesn’t always mean rates are going up. But typically, rates will go up to counteract rising inflation.6)

Instead of swiping more, use this as incentive to go through subscriptions and other recurring charges. Figure out which ones you don’t need (or aren’t even using) and cancel them. Even a few extra dollars a month can help ease the pinch on your finances.

Download your subscription

tracker

Grab this download to help you track what

recurring expenses you’re paying

for.

Get my Download(Opens in a new window)

- https://fortune.com/2022/07/23/how-much-grocery-prices-have-gone-up-with-inflation/(Opens in a new window)

- https://www.freep.com/story/life/food/2022/09/13/grocery-prices-inflation/69491845007/(Opens in a new window)(Opens in a new window)

- https://medium.datadriveninvestor.com/inflation-dont-panic-do-this-instead-601b1f8cd70c(Opens in a new window)

- https://www.scientificamerican.com/article/poor-choices-financial/(Opens in a new window)

- https://consumer.ftc.gov/articles/multi-level-marketing-businesses-pyramid-schemes#:~:text=Most%20people%20who%20join%20legitimate,leaves%20them%20deeply%20in%20debt(Opens in a new window).

- https://www.experian.com/blogs/ask-experian/are-debt-relief-programs-legitimate/#:~:text=High%20fees%20mean%20that%20debt,your%20federal%20income%20tax%20bill(Opens in a new window).

- https://www.investopedia.com/ask/answers/12/inflation-interest-rate-relationship.asp#:~:text=In%20general%2C%20higher%20interest%20rates,rates%20to%20stimulate%20the%20economy(Opens in a new window).

Other Saving and Budgeting articles you may be interested in

-

Recent grad taking a photo with family memberSaving and Budgeting

Am I Saving for My Kid’s Future the Right Way?

529 Plan or Trust? Which is better for your child’s future? Get the definitive breakdown of each savings tool. Find confidence in how you’re planning for your children. -

Buying GroceriesSaving and Budgeting

Top 6 Ways to Save Money on Groceries

Ever experience that, “I’m sorry, how much?!” moment in the grocery store? You know – the one that makes you look back at your cart and wonder how so little could cost so much?