What is a credit score

In technical terms? Your credit score is a mathematical assessment of the likelihood you will repay what you borrow. What that really means: your score tells a lender whether they should loan you money. A higher score makes you more likely to get approved and get a better interest rate. A lower score means you may have a harder time getting approved – and your interest rate will be higher.

How do credit bureaus figure out my credit score?

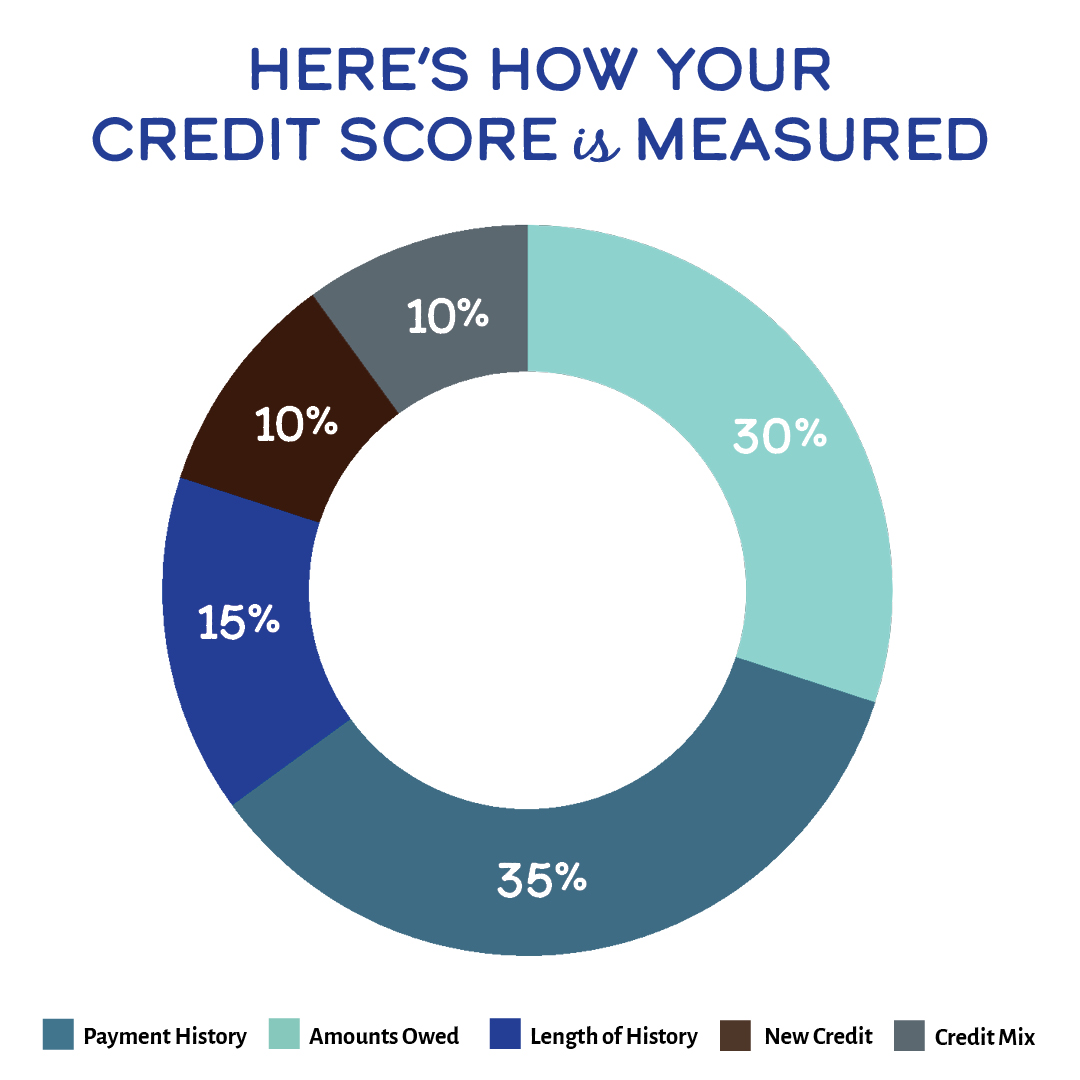

There are three main credit bureaus: Experian, Equifax, and TransUnion. These three organizations collect financial information, including what loans or credit cards you have, how well you pay them, how much you owe on each, and how long you’ve had them. Using this information, they calculate your credit score. While there may be slight variations in how each bureau calculates your score, it’s generally determined by:

- Payment history (35%) Your payment history refers to how often you make late payments. Since this is the biggest piece of your credit score, it’s critical to make on-time payments…even if you can only make the minimum payment.

- Amounts owed (30%) What’s the total amount you owe? The higher the number, the more it will bring your score down. It’s important to avoid carrying large balances on your credit cards.

- Length of credit history (15%) The longer your credit history, the better. Even if you plan on never using your first credit card again, keep the line open as it establishes your history.

- New credit (10%) How often are you applying for and opening new credit? Too many inquiries from lenders can negatively impact your score. Checking your own score, though, won’t. Also, auto loan and mortgage inquiries within a 45-day period are considered as a single inquiry.

- Types of credit (10%) Having a mix of credit shows responsible money management. A combination of term loans, like a car or personal loan, and revolving credit, like a credit card, can help your score.

How is my credit score different than my credit report?

Your credit score is not the same as your credit report – but both are important. Your score is your overall grade. Your report contains the details behind that grade. Each of the three bureaus maintain their own credit report on you. This report contains information about your financial history:

- Your personal information

- Your account information, such as name of lender, payment history, credit limit, amount owed, and years active

- Inquiries, including who’s pulled your credit and when

- Public records, including bankruptcy, liens, and foreclosures

The reports maintained by the bureaus won’t always match. And they can contain errors. Each year – or before a major purchase like a car or home – you should check your credit report from all three bureaus. If you find any inaccuracies, contact them to have it fixed. Errors on your report could impact your ability to get a loan.

Are there different types of credit scores?

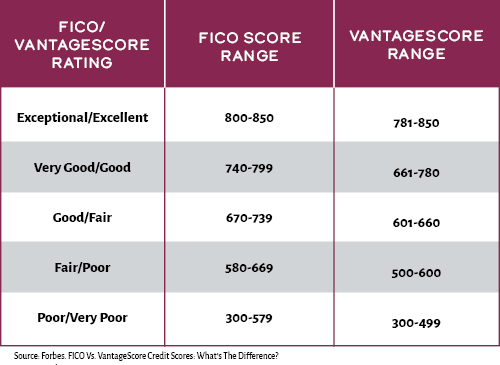

When anyone references their credit score, they’re probably talking about their FICO score…even if they don’t know that.

Your FICO score is your most common score and the one calculated by the three major credit bureaus and it’s based on the scoring model issued by the Fair Issac Corporation.

Why is my credit score different than what my bank sees?

Your FICO score ranges from 300 to 850. The higher the score, the more likely you are to be approved for a loan – and the better your interest rate. The lower your score, the harder it will be to get approved. And your interest rate will only go up.

Another modeling system – VantageScore – is also used. Very often, credit tracking services like Credit Karma use the VantageScore model. Both scores rely on the 300 to 850 range, and both look at the same criteria in assigning a score. The weight given to each criteria, though, may differ between the two methods. This slightly skews how high a VantageScore you may need to qualify for a loan. In other words, if your credit tracker gives you a VantageScore, but your lender relies on FICO scores to make lending decisions, you may not get the interest rate you were expecting.

It’s also easier to start building your VantageScore. To qualify for a FICO score, you must have one tradeline item (loan, line of credit, credit card) open for at least 6 months. VantageScore, on the other hand, just requires that you have one tradeline item open.1

FICO vs. VantageScore: How They Stack Up Against Each Other

But Why Does My Credit Matter So

Much?

Your credit is like your reflection: it’s going to be with you forever. And it can open – or close – doors (sometimes, literally). You may already know that your credit impacts how likely you are to qualify for a loan. This includes car loans, personal loans, credit cards, lines of credit, and mortgages. Your score is also going to determine the interest rate you get. The higher your score, the better your rate.

So why does that matter?

A lower interest rate means your monthly payment will be lower. And, on the flip side, a higher rate will make your monthly payment higher. So, in a very real way, a low credit score will cost you money.

Getting your first credit card? Do these

things.

Landlords and property managers also reference credit reports when you submit an application for an apartment. If your report shows a history of late payments or a foreclosure, they may not rent to you. Utility companies and insurance companies may also request your credit report, although state laws vary on their ability to access and use it.2

And think about this: buying a car or house is stressful enough. Worrying about whether your credit is going to prevent you for either of those is an added stressor you don’t need. Focus on healthy credit habits from the beginning: don’t spend more than you can afford, pay all your bills on time every time, and use credit responsibly.

PUT A CREDIT EXPERT IN YOUR OWN CORNER

MHV members can access certified financial professionals to navigate credit reports, manage debt, even understand renting and home buying.

How do I get my score? How often should I check it?

You’re entitled by law to a free credit report from each of the three bureaus every year. It’s easy to request them here(Opens in a new window). Requesting your credit report doesn’t impact your score. Make a yearly reminder to check your report for any inaccuracies. Remember, your report may differ across the bureaus so check it from each one. And contact them right away if you notice an error.

To stay on top of your credit score, there are several trackers you can use. Many lenders, banks, and credit unions also include a credit score monitoring tool with your account. You should regularly monitor your score, especially if you plan on applying for any credit in the near future. You may also want to sign up for a credit monitoring service. This service will alert you if anyone applies for credit in your name.

WANT GREAT CREDIT? DON’T MAKE THESE MISTAKES.

Can I Change My Credit Score?

Your credit score is entirely in your hands. Sometimes emergencies mean we need to take on debt or use our card more than we like, but with planning and discipline you can almost always repair your credit without outside help.

And the fact is, it’s your daily habits that will make the biggest impact on your score.

Here’s how you might be hurting your credit score

Paying bills late. This is the single biggest mistake to make. Payment history is the biggest piece of your score, and late payments can knock your score down. If you’re struggling to make a payment, contact your lender or card company before a payment is late to ask for help. They will have programs in place to assist you.

Carrying balances. The availability of credit is another piece of your score, and if you’re carrying balances it means less credit is available to you. It also makes financial sense – no balances means no monthly payment.

- Applying for too much credit. Bureaus look at how often you apply for credit and how many credit accounts you open. A few here and there isn’t going to hurt you, but too many too often can bring your score down.

HERE’S THE TRUTH ABOUT IMPROVING YOUR CREDIT SCORE.

Here’s how you can improve your credit score

- Pay bills on time every time. It’s a must. Even if all you can pay is the minimum payment, pay every bill on time. It’s the single biggest piece of your credit score. It also saves you from falling behind and paying late fees.

- Use your card but pay your balance in full. You should use your credit card because usage helps your score. But don’t charge more than you can pay off each month (unless you’re faced with an emergency). Doing so establishes great credit history and saves you from paying interest each month.

- Pay off credit card debt. If you’re like most Americans, you already have credit card debt. Sometimes it’s unavoidable. Work on a plan to help you pay that debt down. It’s OK to reach out to your bank or credit union for help. They will have resources to guide you on debt management. Paying off those balances increase how much credit is available to you, and that boosts your score. It also saves you money!

How do I Contact the Credit Bureaus?

Equifax(Opens in a new

window)

Contact Equifax(Opens in a new

window)

Experian(Opens in a new

window)

Contact Experian(Opens in a new

window)

TransUnion

Contact

TransUnion(Opens in a new

window)

- Forbes. FICO Vs. VantageScore Credit Scores: What’s The Difference?(Opens in a new window) Accessed Jan. 11, 2023.

- Credit.com. How Credit Impact Your Life.(Opens in a new window) Accessed Jan. 11, 2023.

Other Credit, Loans and Debt articles you may be interested in

-

Couple applying for a personal loanCredit, Loans and Debt

Can I Spend My Personal Loan on Anything?

Can you really use a personal loan for anything? Just about. Here’s how personal loans work, why they’re often better than credit cards, and the 4 most common uses. -

Couple looking concernedCredit, Loans and Debt

Does Refinancing Impact my Credit Score?

Ever thought about refinancing your car loan or mortgage? Then you’ve probably wondered what will happen to your credit score if you do refinance. -

family looking at documentCredit, Loans and Debt

Personal Loans vs. Lines of Credit

So you need a Personal Loan. Or do you need a Personal Line of Credit (LOC) Aren’t they basically the same thing? Not exactly, and understanding the key differences will be important in determining which is the better option for you. Let's run through three of the biggest differences between Personal Loans and Lines of Credit.