Understanding Deferments, Forbearances, and other Financial Hardship Solutions

Navigating financial hardships is intimidating enough, and trying to understand the various options and terminology only makes asking for help feel scarier. But help for both consumer loans – things like car loans, personal loans, and credit cards – and mortgages is available and lenders are always willing to work with you. It is important to them to help you maintain financial health, and the type of assistance offered will depend on whether you’re facing a short- or long-term hardship.

Hardship assistance options vary from lender to lender. While many banks and credit unions offer the programs outlined in this article, please keep in mind that how each program is administered will vary. This article specifies MHV’s approach to financial hardship assistance programs and is intended for guidance purposes only. We encourage you to speak with a representative if you have specific questions.

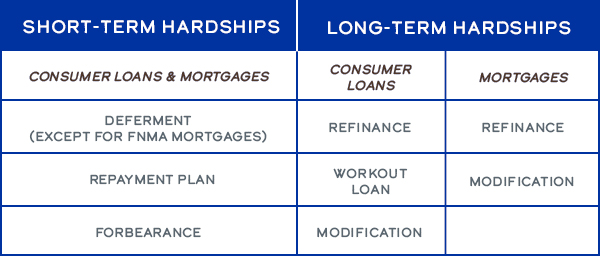

Solutions for Short-Term Financial Hardships

Deferments for Consumer Loans

If you cannot pay your car loan or personal loan your financial institution may be able to offer you a deferment. A deferment is an agreement between you and the lender to reduce or postpone your payment for a designated period of time. Typically, a deferment will not last longer than 90 days. The deferment extends the life of the loan by an equal length of time.

For example, if you apply for and receive a 90-day deferment, the term of your loan will extend by 90 days. Since credit cards are revolving accounts, and don’t have a specific term, a deferment on a credit card is simply an opportunity to skip the agreed number of payments.

For personal and auto loans, interest will likely still accrue throughout the deferment period. Because the term extends, however, your payment won’t go up to recapture the interest. Essentially, the deferments shifts your current obligations to the end of your loan. With credit cards, interest is also still charged and will continue to be added to your card balance.

Deferments for Mortgages

If you’re facing a short-term hardship and are unable to pay your mortgage, deferment may also be an option. Similar to consumer loans, deferments for mortgages are based on an agreement with your lender to postpone payments for a predetermined period of time. Unlike consumer loans, however, MHV does not extend the term of your mortgage. This means that you will be responsible for paying the amount owed when your mortgage matures or if you pay the mortgage off sooner, whichever happens first.

Throughout the deferment period, you generally need to make your escrow payments. If not, your escrow balance will be drawn negative as your lender continues to make your tax and/or homeowner’s insurance payments. This could result in a substantial increase in your monthly payment to make up that negative balance.

While interest does accrue throughout the deferment period, MHV will calculate that interest separately from your principal payments. This helps to protect you from being charged interest on the interest.

Does a deferment hurt my credit?

If there is no payment due, your loan or mortgage will not show as delinquent on your credit report. For consumer loans, the deferment takes your current payments and moves them to the end of your loan by extending your term. For mortgages, the deferred amounts are set aside until maturity or payoff. Since there are no payments coming due during the deferment period, you’re not falling behind on them and your credit is not impacted.

It’s important to note that a deferment is an agreement with your lender or financial institution. Skipping payments without a prior agreement will have a negative impact on your credit score(Opens in a new window).

How does a deferment help me?

By postponing your payments, you relieve yourself of a financial obligation while you deal with your hardship…without hurting your credit. It gives you breathing room to get yourself back on solid financial footing. Because deferment protects you from delinquency or charge-off, it also helps you to protect your credit.

What if I don’t qualify for a deferment because I’ve already missed too many payments?

If you don’t qualify for a deferment because you’ve already missed too many payments, meaning your loan or mortgage is already past due, your financial institution can work with you on a payment plan. These individualized plans are typically an informal agreement to help you catch up and become current on your loan.

For consumer loans and mortgages, this usually means paying a bit more each month until the past due amount is paid in full. Lenders will usually not allow payment plans to exceed 12 months; if, for example, the mortgage payments cannot be caught up within a year, solutions for a longer-term hardship are used.

Payment plans are not always formal agreements. They won’t protect your credit because your loan will already be reported as delinquent and will continue to report as delinquent until the past due amount is satisfied. Payment plans are a great option, however, to help get you back in good standing and start improving your credit.

Delinquency is not the same as being in default. Delinquency indicates that you are late on your payments. Being in default, on the other hand, is more serious and indicates an inability to pay back the loan according to the agreed upon terms.

Payment plans can usually be worked out at any point the loan is delinquent so it’s important to reach out to your lender or financial institution no matter how far behind you feel you are. Initiating the conversation can help you avoid a charge off, which will take a serious bite out of your credit score and damage your relationship with your lender.

Short-Term & Long-Term Hardship Assistance

Solutions for Long-Term Financial Hardships

Loan Modifications, Refinances, and Workout Loans for Consumer Loans and Mortgages

If you’re faced with a long-term financial hardship, deferring your consumer loan or mortgage may not be an option. Financial institutions like MHV offer refinances, loan modifications and workout loans to support people with long-term hardships.

Many community banks and credit unions have an individual employee or group of employees dedicated to reviewing long-term financial hardship requests. These employees are responsible for assessing the request, reviewing potential solutions, and approving the most ideal one.

A refinance is when the balance of your loan is rewritten over a new term, and potentially with a new interest rate, therefore lowering the monthly payments. Refinances are subject to credit approval. A refinanced loan with lower payments grants you more manageable payments while working through a long-term financial hardship.

A workout loan is similar to a refinance in some ways. A workout loan also rewrites the balance of your loan over a new term, and potentially with a new interest rate, therefore lowering the monthly payments. However, the difference between a workout loan and a refinance is that a workout loan is granted as an exception outside of the credit union’s normal lending guidelines, and is not necessarily subject to credit approval. As such, additional information or documentation may be required to demonstrate the financial hardship that exists.

A loan modification provides changes to any aspect of the original loan terms. This can include changing the interest rate, extending the term, and reducing the payment. Loan modifications sometime require a trial period before the modified terms of the loan are made permanent. This trial period allows both you and the lender to gauge your ability to pay under the new loan terms.

Will a loan modification hurt my credit?

Whether or not a modification impacts your credit depends on how the modification is written and the status of your loan prior to modification. If your modification requires a trial period, yes, your credit will reflect the delinquent status of your loan until the probationary period is over. Once the modification is made permanent, however, your credit report will reflect the new terms of your loan and thus your loan will no longer show as delinquent. Additionally, if your loan was delinquent going into the modification, those delinquent marks from their missed payments will remain on your credit and will be reflected in the payment history of that loan or mortgage.

Forbearance

Forbearance is a solution associated with mortgages or consumer loans that protects you from collection calls, repossession, or foreclosure during the term of the forbearance. Forbearance is an agreement with your lender that allows you to temporarily stop your loan or mortgage payments.

For mortgages, deferments require you to continue to make escrow payments. If you enter into forbearance, however, you do not need to pay into your escrow. The financial institution continues to make your tax/homeowner’s insurance payments out of your escrow account, drawing it negative if need be.

Your lender may decide to offer a forbearance with reduced payments rather than no payments. In this scenario, your reduced monthly payments are held in an account for you; once enough has been collected to make a full loan or mortgage payment the lender applies those reserved funds. If you can afford to make reduced payments, this option prevents you from falling too far behind on your loan or mortgage.

It’s important to note that with a forbearance your payments continue to become due during the term of the forbearance, even though you’re being allowed to temporarily stop making your payments. This means that at the end of the forbearance, these payments will still be due. Once your hardship is resolved, your lender will work with you to develop a plan to begin paying your mortgage again and catch up on past due payments.

Does forbearance hurt my credit?

Because you’re not making any payments on your loan or mortgage, it will reflect as delinquent on your credit. This will impact your score. A forbearance protects you from collection attempts, repossessions, or foreclosure, though, which is a far more significant ding to your credit and damaging to your relationship with your lender.

What’s the best solution for me?

Your absolute best option if you are facing financial hardship is to contact your financial institution, lender, utility company, and other service providers. These companies work with individuals every day to help them through difficult periods and, as long as you are open in your communication with them, will be willing to work with you.

It is common to feel embarrassed or even scared when you have to discuss your financial situation but if your financial institution and other lenders aren’t aware of your hardship, they will never be able to offer you solutions. Whether that solution turns out to be a deferment, modification, or other assistance program, it must begin with a conversation.

Other Credit, Loans and Debt articles you may be interested in

-

Couple applying for a personal loanCredit, Loans and Debt

Can I Spend My Personal Loan on Anything?

Can you really use a personal loan for anything? Just about. Here’s how personal loans work, why they’re often better than credit cards, and the 4 most common uses. -

Couple looking concernedCredit, Loans and Debt

Does Refinancing Impact my Credit Score?

Ever thought about refinancing your car loan or mortgage? Then you’ve probably wondered what will happen to your credit score if you do refinance. -

family looking at documentCredit, Loans and Debt

Personal Loans vs. Lines of Credit

So you need a Personal Loan. Or do you need a Personal Line of Credit (LOC) Aren’t they basically the same thing? Not exactly, and understanding the key differences will be important in determining which is the better option for you. Let's run through three of the biggest differences between Personal Loans and Lines of Credit.