Home Equity Loan or Line: What’s better for me?

One of the first steps in applying for a Home Equity Loan or Line of Credit (HELOC) is determining which is better for you. Our article will compare Home Equity Loans and Home Equity Lines of Credit for you, helping you identify the advantages and disadvantages of each. Then you can assess the pros and cons of each, and measure them against your plans, budget and requirements.

Compare Home Equity Loans and HELOCs

Why choose a Home Equity Loan or Line of Credit over other loan types?

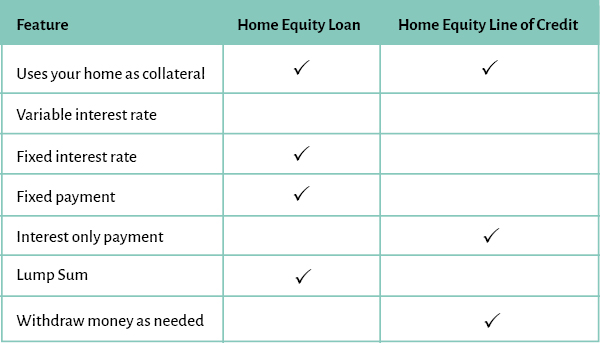

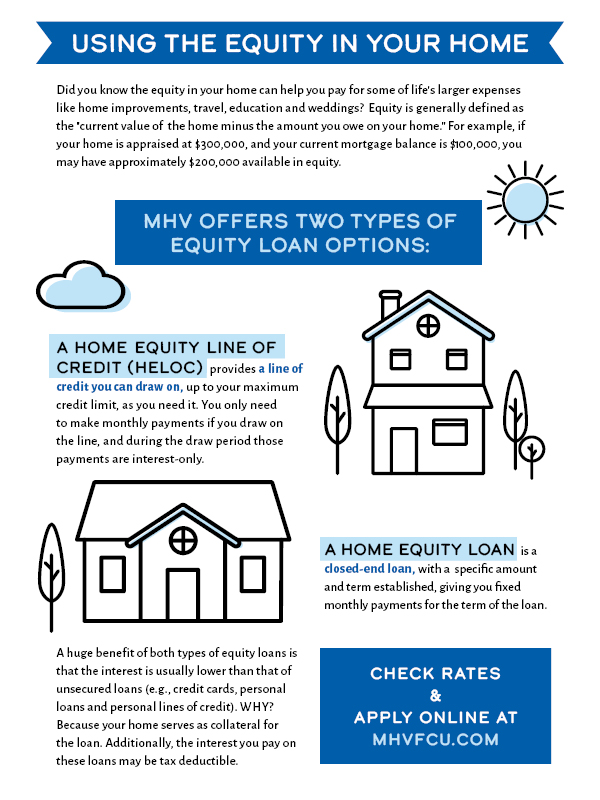

The benefit of a Home Equity Loan or Line of Credit comes from the fact that these products are secured by your home’s equity. Because of this, these products will typically carry a lower interest rate than an unsecured Personal Loan. Lower interest rates can save you hundreds, even thousands, of dollars over the life of the loan. In addition, the fact that these products use your home as collateral allows you to borrow more money than you usually can with a Personal Loan, making big-ticket purchases possible. This makes Home Equity Loans and Home Equity Lines of Credit appealing when you need funds for things like home renovations or tuition costs.

What are the pros and cons of a Home Equity Loan?

The advantage of a Home Equity Loan centers around its interest rate and its payment, both of which make it a better choice for you if you have a definitive plan for the money.

► Fixed interest rate

Home Equity Loans are similar to other types of loans in that you will be approved for a certain amount at a specific interest rate. The interest rate(Opens in a new window) you are approved for is fixed, meaning it will not change throughout the life of the loan. The interest rate you are approved for will depend on a variety of factors, including your credit score and your debt-to-income ratio (DTI)(Opens in a new window).

► Fixed monthly payment

Because the interest rate on a Home Equity Loan is fixed, your monthly payment won’t change,

provided you don’t accrue any late fees. This can be important because having a fixed monthly

payment makes it easy to budget for your Home Equity Loan payment. With a fixed payment, you can

plan for exactly how much you’ll need for the payment each month.

There are disadvantages

to a Home Equity Loan, too. Because it is a loan, you will receive the full amount of your

equity up front. You won’t have the equity left, or only a very minimal amount, to use for

future expenses or emergencies. Furthermore, this could be a potential issue if your home

depreciates in value.

What is a Home Equity Loan Best For?

Home Equity Loans are best for people who prefer fixed payments and who know exactly how much money they are going to need to borrow. Typically, the amount needed for large home improvement projects or education expenses will surpass what is available via a personal loan, and be too large to put on a credit card. That makes a Home Equity Loan an attractive alternative.

What are the pros and cons of a HELOC?

A Home Equity Line of

Credit has advantages, too. Because it is a line of credit and not a loan,

you can draw the amount of money you need as you need it, up to your available line. This gives

you the flexibility to fund projects and other expenses as you go, rather than getting the

entire amount up front. Another benefit of HELOCs is that, during the draw period, your payments

are typically interest-only, and if you haven’t used any of your line then you don’t have any

payments at all.

The drawback of a HELOC is that the interest rate is variable. This

means that if rates rise, your payment will go up. This makes it harder to budget for your HELOC

payment. Another potential issue with a HELOC is that, with the full amount of your line at your

disposal, it can be tempting to tap into it for items or purchases that aren’t really

necessities, potentially putting yourself into a stressful financial situation.

Who is a HELOC best for?

HELOCs are probably a better option for people who simply aren’t sure how much money they are going to need or when exactly they’ll need it. Whether you are doing an extensive house renovation that will require several projects over time, or you just want the peace of mind of knowing the line of credit is available to you in the event of an emergency, a HELOC is a good option for its flexibility.

Watch our video on the differences between a Home Equity Loan and a HELOC

Once you determine which is the best choice for you, you’re going to want to determine the current value of your home. Once you actually apply for a Home Equity Loan or a HELOC you will need to have your home appraised, but websites like Zillow and Trulia can provide you with current estimates. This will help you get an understanding of how much you may be able to borrow. From there, it’s simply a matter of applying for your Home Equity Loan or HELOC and gathering the necessary documents. To figure out if a Home Equity Loan or a Home Equity Line of Credit is better for you, consider your plans for the money, interest rates, and your personal budget. Look at the advantages and disadvantages outlined in this article to see which option best aligns with your needs.

Other Home articles you may be interested in

-

Couple refinancing their home for projectsHome

Are Mortgage Refinances or Home Equity Loans Better?

One of the biggest advantages to owning your home is the ability to tap into the equity you build, or the amount of your house that you’ve paid off. When you need to access that equity as cash, though, you’re faced with a couple of options. -

A nice houseHome

Here's What Your Home's Equity Can Be Used For

What can you do with the equity in your home? Find out how to use it, which is better, and how to qualify for either. -

Couple speaking to a mortgage expertHome

Home Buying Tips Straight From the Experts

5 insider tips from mortgage officers. Find out what advice they would give you about buying a house. And find out why it’s normal to feel overwhelmed.