Where it All Began

We’ve come a long way from metal plates.

Back in the early 20th century, Western Union started issuing metal plates that people could use to defer payments – one of the first renditions of today’s credit card. These metal plates were only available to a select group of consumers, though. It wasn’t until the “Charg-It Card” hit the scene in 1946 that we have an example of something like today’s credit card. A few years later, the Diners Club was created…and the modern-day credit card was born.1

And now you’re ready for your first credit card. And that means you’re ready for some knowledge on how to use it – responsibly – to build your credit.

Getting Started with Your First Credit Card

SECURED CREDIT CARDS

Your first credit card(Opens in a new window) doesn’t have to be a secured card. But if you haven’t established any credit yet, it can be hard to get approved for a standard unsecured card. Lenders are hesitant to allow someone to spend borrowed money (which is what credit is) when that person hasn’t proven their ability to pay it back.

Secured cards, though, are made specifically for people who are just building their credit or need to rebuild it after bankruptcy or financial hardship.

THE FAST OVERVIEW OF SECURED CREDIT CARDS

Grab

this download for the 10-second overview of how secured credit cards work. Get My Download(Opens in a new window)

So what’s the difference? A standard credit card is unsecured: Your bank or credit union is letting you borrow money without providing any collateral. A secured card, however, is protected by your own money. This makes it easier to get approved (often you just need proof of income) and allows you to start practicing responsible credit usage – and build your credit score.

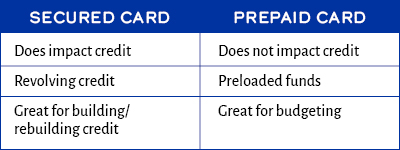

Secured cards are not the same as prepaid cards. Prepaid cards are not credit cards and do not contribute to building credit history.2 Prepaid cards are great for learning to budget your spending but are not reported to credit bureaus.

Collateral is something a lender uses to protect themselves in the event you can’t make payments. A car loan, for example, uses the car as collateral. If you can’t pay, the lender can repossess the car to make up for the money they lent you. An unsecured loan does not require collateral.

When you apply for a secured credit card, the issuer will require you to have a certain amount of money reserved in your savings. For example, if you apply for a credit card with a $500 limit, the bank or credit union may require you to have $600 or more on hold in your savings.

This collateral protects the issuer in the event you are unable to make your payments. Keep in mind: making late payments or failing to make payments on a secured card will have a negative impact on your credit score. Even though the card is secured, it is your responsibility to make on-time payments.

CHANGING TO AN UNSECURED CARD

Your bank or credit union may allow you to transfer to a traditional unsecured card after a certain period of time. Typically, you’ll have to make consistent on-time payments for at least a year before you’re eligible for an unsecured card.

FIRST CREDIT CARD? DO THESE THINGS.

Get the

expert’s tips on how to manage your first credit card in this 7-minute video. Watch Now(Opens in a new window)

If your credit card company doesn’t offer the ability to transfer to an unsecured card, you’ll have to apply for one. Keep your secured card open – even if you’re approved for the unsecured card. Even if you don’t use it, it demonstrates credit history to the credit bureaus. They look favorably on longer credit history.

Manage Your Credit Card like a Pro

The most important thing to remember about credit? It is borrowed money. If you can’t afford something without credit, you probably shouldn’t buy it. Following this rule will teach you responsible credit usage – and save you from tremendous credit card debt. Obviously, emergencies happen. And in those situations, it’s good to have credit to fall back on. But for everyday purchases, only spend what you can afford to pay off.

Secured cards look and operate just like a traditional unsecured credit card. Instead of paying with cash or a debit card, you use the credit card to complete your purchase. Once you use the card, you owe that amount to the card issuer. If that amount is not paid in full, you will also owe interest.

You do have to use the card, though, to build credit. Simply having a card doesn’t do anything. It’s the act of using and repaying the credit that will build your history and score. Here’s a simple action plan to get you started:

- Buy your groceries or another small purchase with your credit card – but only spend what you can afford to pay with what’s in your checking account.

- The next day, check your card balance. Note how that purchase is now reflected in your balance.

- Make a payment to your credit card company covering that purchase in full.

This action plan does two things for you. First, it gets you in the habit of using your credit card to purchase things you can afford – not to buy things outside of your price range. It also builds the habit of paying your balance in full each time. Paying your balance in full each month saves you money by avoiding interest charges.

Payments Matter…a Lot

Whether your first card is secured or unsecured, how you manage your payments is critical to your credit health.

Ideally, you should pay the full balance of your card each month. (That’s why it’s so important you don’t overspend on your credit card.) Paying your balance in full each month saves you from ongoing interest charges. It also keeps your capacity – or how much available credit you have – at a max. High capacity helps build your credit score.

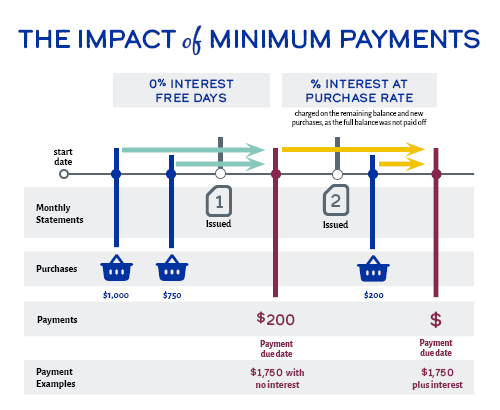

If you can’t pay the full balance, pay as much as you can. At the very least, you must make the minimum payment. The minimum payment is the lowest amount the credit card company will accept. Try to avoid the habit of paying just the minimum amount due. The majority of your minimum payment covers the interest, not the balance you owe. Making the minimum payment means you’ll carry a balance on your card for a long time. Even paying a little more than minimum is better.

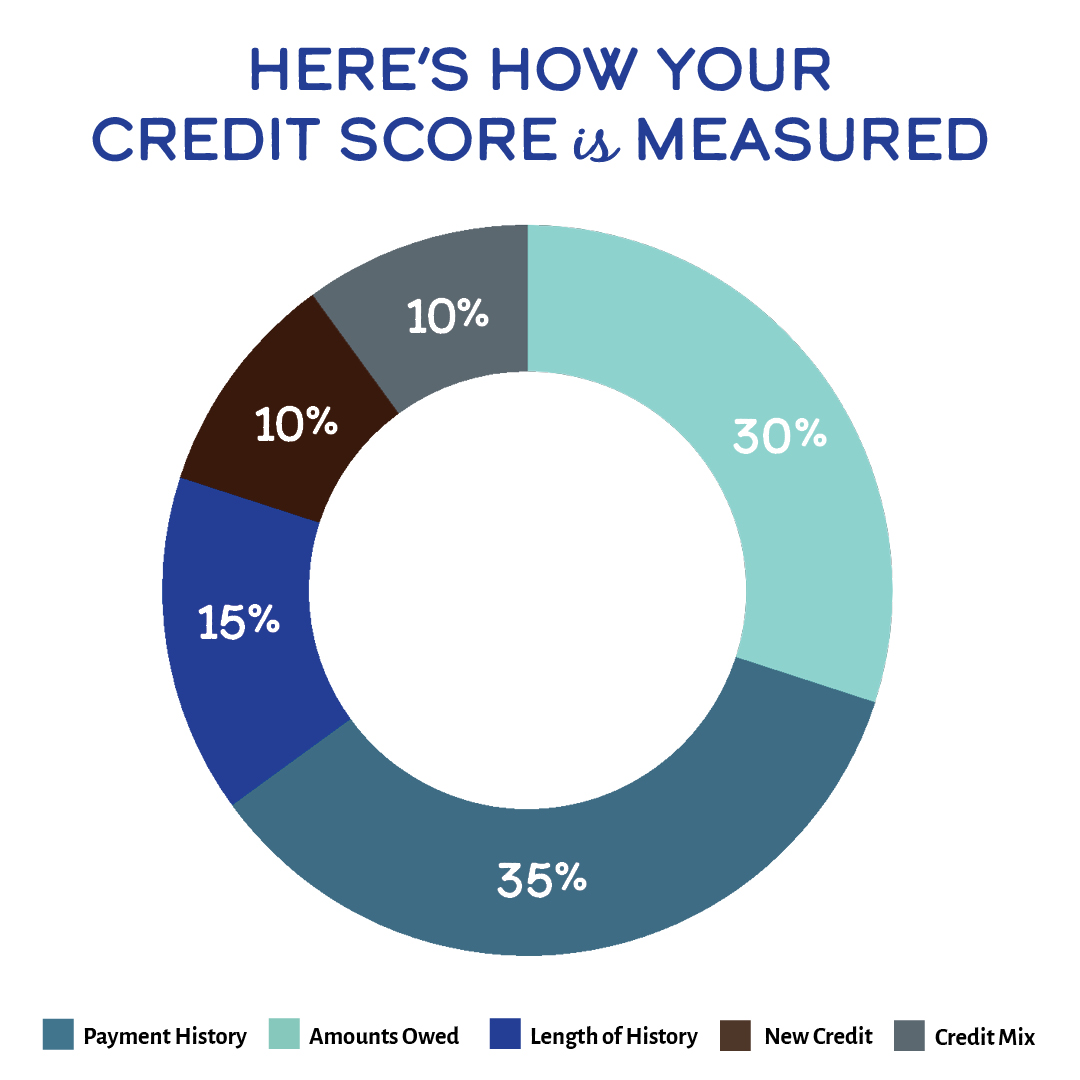

Always make your payment on time. Making on-time payments is critical to building a good score: payment history is the single biggest factor bureaus consider. Late payments will also result in a fee. According to CreditCards.com(Opens in a new window), your first time paying late, the most an issuer can charge you (as of 2022) is $30. But if you miss another payment due date within six billing cycles, you can expect to pay up to $41.

Practical ways to use your credit card to build

credit

Credit cards can help you build or rebuild your credit. But you must use them responsibly to keep pumping up your score.

1. Keep your oldest card open

Don’t close your credit card once you

build your score. Credit history is one of the factors the bureaus look at when determining your

score. The longer your history, the better. Even if you don’t plan on using the card, keep it

open.

2. Have a mix of credit

You don’t need multiple credit cards to build

your score – it won’t necessarily build your score any faster. Once you have established credit,

though, having a mix of credit can help your score. This could include a credit card and a car

loan, for example. The credit card demonstrates your ability to manage revolving credit. The

loan demonstrates your ability to manage an installment loan.

3. Make your payment on time, every time

Payment history is the biggest

factor impacting your credit score. Making your payment on time is critical to building and

maintaining a good credit history. If you’re ever in a position of being unable to make a

payment, reach out to your bank or credit union before the payment is late. They will be

able to assist you.

4. Pay your balance in full

Credit is borrowed money. To avoid interest

charges piling up and starting a never-ending cycle of credit card debt, only use your card for

items you can afford to pay off. Responsible credit usage isn’t an invitation to buy whatever

you want. It’s an opportunity to learn effective money management.

WANT GOOD CREDIT? DON’T DO THESE THINGS.

Our

credit expert is back in this 13-minute podcast episode to dish on every day habits that destroy

credit scores. Listen Now(Opens

in a new window)

Caution: Avoid these credit mistakes

Here’s your chance to learn from others: these credit mistakes are common, but they can cause long-term financial repercussions.

1. Maxing out your credit card…and then making minimum payments

Maxing out your card means you spend it all. Whatever your credit limit is, you use all of it. This is a bad choice for a couple of reasons. First, you now owe whatever that amount is. Plus interest. Second, you don’t leave any available credit to use in the event of an emergency.

2. Relying on grace periods

Installment loans such as car or personal loans typically have a grace period. A grace period is a length of time after the due date during which you won’t get a late fee. For example, if your car loan has a 10-day grace period, you can make your payment up to 10 days late without a late fee. Credit cards are not installment loans. They are revolving credit. And they don’t have grace periods. You need to make your payment by the due date, every time.

3. Getting the card and not using it

Simply having a credit card doesn’t build your credit because you’re not demonstrating responsible usage. It’s how you use and repay the money that impacts your score. Use the card wisely – only charging what you can pay off – and pay it off by the due date every time. This kind of money management is what the bureaus look at when calculating your score. And remember to keep the card open. Longer credit history works in your favor.

4. Introductory rates

Introductory rates are designed to tempt you into a new credit card. They are low – often 0% APR – and convince people they can save money. And if you can pay off the balance before the introductory rate expires, they can save you money. Problems start, though, when the balance isn’t paid off and the rate jumps up after the introductory period.

- https://www.bankrate.com/finance/credit-cards/the-evolution-of-credit-cards/

https://wallethub.com/answers/cc/prepaid-vs-secured-credit-card-2140743246/#:~:text=The%20main%20difference%20between%20prepaid,while%20prepaid%20cards%20do%20not

Glossary of Credit Terms

- Issuer: the company that issued your credit card, typically a bank or credit union. Some major retailers also issue credit cards.

- Credit limit: the maximum amount you can charge to your credit card. Your credit card company can increase or decrease the limit based on your credit score.

- APR: annual percentage rate. The amount of interest you’ll be charged for using the card. Your rate is set by the credit card company and can increase or decrease. Rates can be variable, meaning they change as the prime rate changes, or fixed, meaning they stay the same.

- Introductory rate: card companies will often offer an introductory rate to entice you to apply. This is a low rate (sometimes 0%) that expires after a set amount of time. Once the introductory rate expires, your standard APR will apply.

- Due date: the date by which your payment is due.

- Minimum Payment: the smallest possible amount the credit card company will accept for your monthly payment. Typically the majority of this amount covers the interest with very little actually going towards your balance.

- Balance: the total amount you owe on your credit card.

- Late fee: an amount of money you are charged if you pay your bill after the due date.

- Balance transfer: moving the balance on one credit card to another. There is sometimes a fee associated with a balance transfer.

- Credit bureaus: a company that collects information about people’s credit history. Bureaus calculate your credit score and create your credit report. The three main bureaus are Equifax, Experian, and TransUnion. Your score and report may not be the same across all three.

- Credit score: the numerical value that predicts how likely you are to pay a loan back on time. The score is computed using a variety of factors including your payment history, the length of your credit history, how much available credit you have, recent credit applications, and whether you have a history of bills going to collection or bankruptcy.

- Credit report: unlike your score, your credit report documents your credit history. It shows your current and past loans and credit cards, your payment history, and any judgments against your credit. Each credit bureau issues its own report and there can be inconsistencies among them

- Capacity: how much credit is available to you. The better your capacity, the better your credit score. That is one of the reasons to avoid maxing out your credit card.

- Max out: when you use the entire available amount of your credit card.

- Billing cycle: the time between two statement closing dates. Any transactions made during the billing cycle are added to any existing balance, plus interest, to determine your current balance owed

- Revolving credit: credit that continues to be available to you after you pay it off, such as a credit card or line of credit.

- Installment loan: credit that is paid back each month and finished once you pay it off. Car loans, personal loans, and mortgages are installment loans.

Other Credit, Loans and Debt articles you may be interested in

-

Couple applying for a personal loanCredit, Loans and Debt

Can I Spend My Personal Loan on Anything?

Can you really use a personal loan for anything? Just about. Here’s how personal loans work, why they’re often better than credit cards, and the 4 most common uses. -

Couple looking concernedCredit, Loans and Debt

Does Refinancing Impact my Credit Score?

Ever thought about refinancing your car loan or mortgage? Then you’ve probably wondered what will happen to your credit score if you do refinance. -

family looking at documentCredit, Loans and Debt

Personal Loans vs. Lines of Credit

So you need a Personal Loan. Or do you need a Personal Line of Credit (LOC) Aren’t they basically the same thing? Not exactly, and understanding the key differences will be important in determining which is the better option for you. Let's run through three of the biggest differences between Personal Loans and Lines of Credit.